Variable Selection in Regression Models Using Global Sensitivity Analysis

Journal of Time Series Econometrics

About

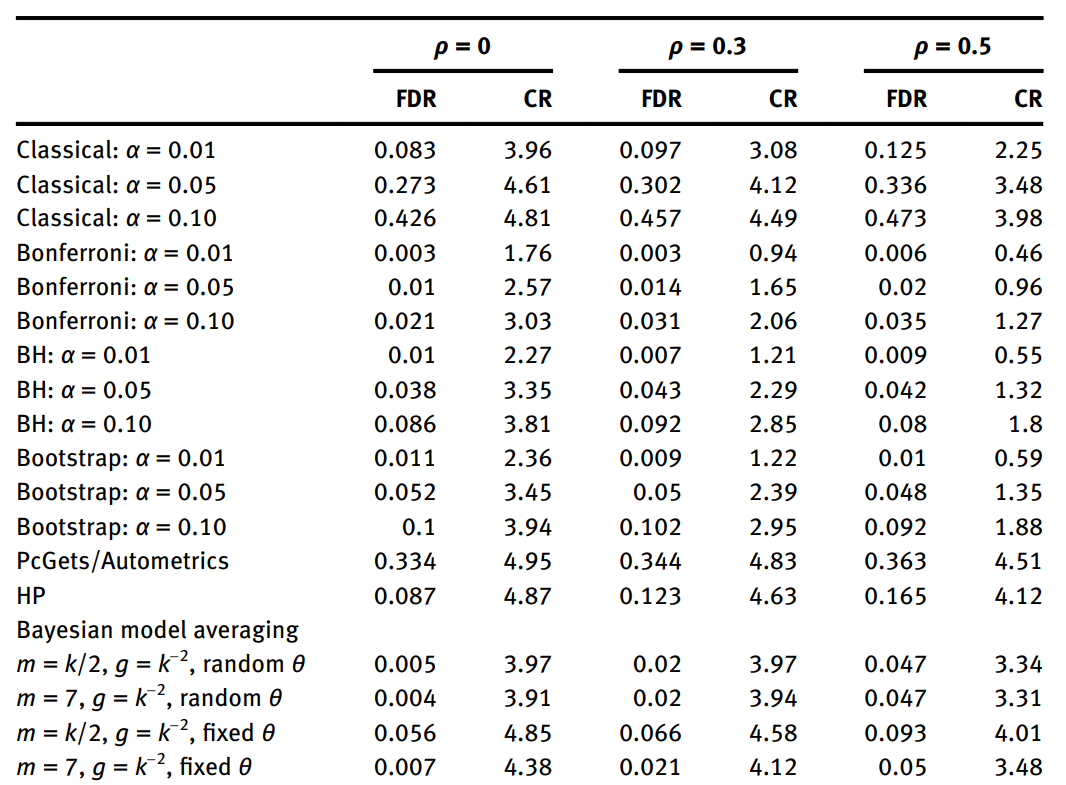

Global sensitivity analysis is primarily used to investigate the effects of uncertainties in the input variables of physical models on the model output. This work investigates the use of global sensitivity analysis tools in the context of variable selection in regression models. Specifically, a global sensitivity measure is applied to a criterion of model fit, hence defining a ranking of regressors by importance; a testing sequence based on the ‘Pantula-principle’ is then applied to the corresponding nested submodels, obtaining a novel model-selection method. The approach is demonstrated on a growth regression case study, and on a number of simulation experiments, and it is found competitive with existing approaches to variable selection.